Personal Income Tax Rates in Indonesia

After understanding the reporting obligations and the subjects of taxation, the next step is to learn about the applicable tax rates. In Indonesia, personal income tax rates are regulated through a clear system, which consists of progressive rates and final rates for certain types of income. Understanding these rates is important so that each taxpayer can accurately calculate their tax obligations.

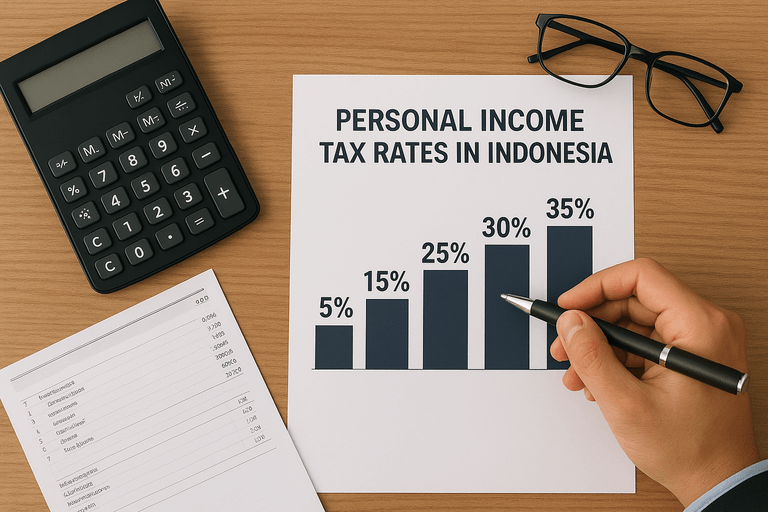

Progressive Income Tax Rates

Progressive rates mean that the higher a person’s income, the greater the percentage of tax imposed. Based on the Law on the Harmonization of Tax Regulations (UU HPP), which has been in effect since the 2022 tax year, the progressive rates for individual domestic taxpayers are as follows:

- Taxable income up to IDR 60 million: 5%

- IDR 60 million – IDR 250 million: 15%

- IDR 250 million – IDR 500 million: 25%

- IDR 500 million – IDR 5 billion: 30%

- Above IDR 5 billion: 35%

This rate structure reflects the principle of fairness, where taxpayers with higher income bear a greater tax burden.

Final Rates for Certain Types of Income

In addition to progressive rates, there are also final rates that apply to specific types of income. These final rates are special and are not combined with other income in the Annual Tax Return calculation. Some examples include:

- Final income tax of 0.5% of turnover for MSME taxpayers with annual turnover up to IDR 4.8 billion.

- Final income tax of 10% on lottery prizes.

- Final income tax of 2.5% on income from certain construction services.

With these final rates, tax calculation becomes simpler because the tax is directly withheld from specific types of income without having to follow the progressive scheme. (Source: Directorate General of Taxes – PPh Final)

Annual Income Tax Return Reporting

Every taxpayer, whether an individual or an entity, is required to submit an Annual Tax Return (SPT) to the Directorate General of Taxes. The SPT serves as a means of reporting income, calculating payable tax, and recording payments made during the tax year. By filing the SPT accurately and on time, taxpayers can avoid administrative penalties and maintain legal compliance. To provide a clearer picture, below is an explanation of deadlines, penalties for late submission, and the steps that need to be prepared in the reporting process.

Deadlines and Penalties for Late Submission

The Annual Tax Return for individual taxpayers must be submitted no later than March 31 of the following year. For example, income earned in 2025 must be reported through the SPT by March 31, 2026, at the latest. If the report is submitted late, the taxpayer will be subject to an administrative penalty of IDR 100,000 for individuals. In addition, if there is an underpayment, interest will be added in accordance with the applicable tax regulations.

How to File the Annual Tax Return

Filing the SPT has become easier since it can now be done online through the e-Filing service available on the official website of the Directorate General of Taxes (Source: Directorate General of Taxes). Taxpayers simply need to log in using their Tax Identification Number (NPWP) and password, then complete the form according to the applicable type of SPT. Once the form is filled in and submitted, the system will issue an Electronic Receipt (Bukti Penerimaan Elektronik or BPE) as proof that the SPT has been officially filed.

Documents Required for Reporting

To ensure a smooth reporting process, taxpayers need to prepare the following documents:

- Tax Identification Number (NPWP)

- Tax withholding slip (for example Form 1721 A1/A2 for employees)

- Reports of other income outside of salary (such as business, rental, or investment income)

- Proof of tax payment or deposit in case of underpayment

- Other supporting documents as needed, such as statements of assets or liabilities

By understanding the deadlines, the reporting procedures, and the required documents, taxpayers can file their Annual Tax Return more easily and avoid administrative penalties.